M&A can create growth, market access, operating scale, and other strategic gains, but the failure record is hard to ignore. Harvard Business Review notes that studies often report acquisition failure rates of 70% to 90%.

PwC also reported that global M&A deal values rose 15% in the first half of 2025, while deal volumes fell 9%. In simple terms, fewer deals were announced, but the ones that moved forward were larger and more difficult to execute well.

So, why do mergers and acquisitions fail? This guide explains the main causes of M&A failure, what failure rate statistics mean, real examples of failed mergers, and practical ways to reduce deal risk, including the role of data rooms in M&A.

Key takeaways

- Why mergers fail usually comes down to weak due diligence, overpayment, poor integration planning, culture gaps, and unclear strategic logic.

- The commonly cited M&A failure rate of 70% to 90% depends on how “failure” is measured.

- A deal can close successfully and still fail later if it destroys shareholder value or misses its synergy targets.

- Failed acquisitions often reveal risks that were visible before closing but were not tested enough.

- Better diligence, earlier integration planning, and clear ownership of post-close work can reduce avoidable deal failure.

- Virtual data rooms for M&A help deal teams manage document review, access rights, Q&A, and audit trails during due diligence.

What is a merger and acquisition (M&A)?

A merger occurs when two companies combine into one entity, though the parties are not always equal in control, value, or influence. An acquisition happens when one company purchases control of another company or its assets; the target may be absorbed, operated as a subsidiary, or integrated only in part.

In simple terms, mergers and acquisitions meaning refers to a business combination or control transfer. A merger typically involves two companies joining to form a single combined entity. An acquisition usually means one company buys another and becomes the controlling owner.

What is the M&A failure rate?

The M&A failure rate is cited as 70% to 90%, but that range needs context. It does not mean that 70% to 90% of deals fail to close. It usually refers to deals that fail to create expected value after closing.

That value test can include several measures: share price performance, return on invested capital, synergy delivery, customer retention, earnings growth, or strategic progress. Because researchers use different measures, the failure rate varies.

This is why the M&A success rate is also difficult to define with one number. A transaction may meet its legal closing conditions but still miss the business target that justified the acquisition.

Why failure rates vary

Failure rates vary because “success” is measured differently across studies.

For example, one study may focus on shareholder returns after the announcement. Another may focus on synergy delivery. A private equity buyer may judge success by exit returns, while a strategic buyer may look at market share, operating margin, or product expansion.

Deal type also changes the picture. A small bolt-on acquisition is usually easier to absorb than a large merger of equals. Cross-border deals add more pressure because legal systems, labor rules, management styles, and customer expectations may differ.

What “failure” means in M&A

A transaction may fail if:

- The buyer pays too much and cannot earn back the premium.

- Synergies take longer than expected or never appear.

- Key customers leave after closing.

- Integration distracts management from the core business.

- Employees lose trust, and important talent exits.

- The acquired company does not support the buyer’s strategy.

In other words, M&A failures are usually value problems. The deal may close, the announcement may sound convincing, and the integration team may work hard. Still, if the buyer cannot convert the acquisition into durable business value, the transaction has missed its purpose.

Perfect data rooms for M&A

Overall rating:

4.9/5

Excellent

Overall rating:

4.8/5

Excellent

Overall rating:

4.7/5

Excellent

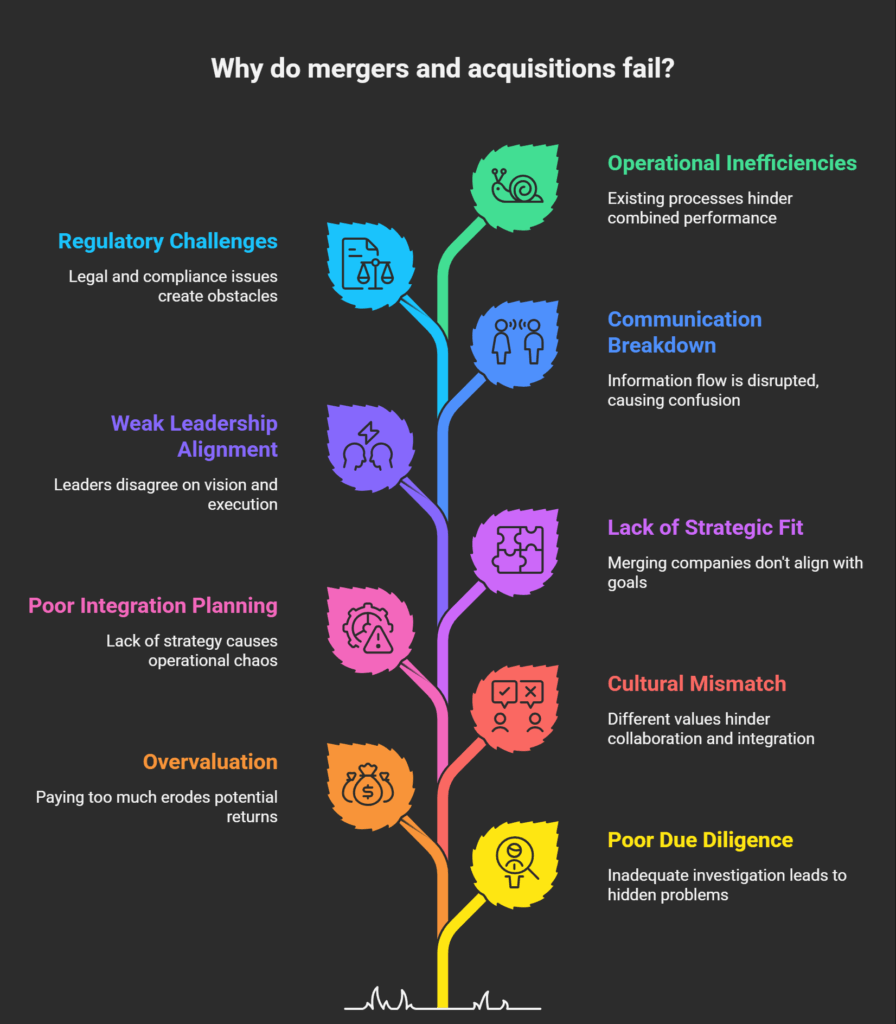

Why do mergers and acquisitions fail?

Most failed acquisitions come from a chain of decisions that looked manageable at the time. These patterns repeat across industries.

Below are the most common reasons mergers fail.

1. Poor due diligence

Poor due diligence is one of the clearest reasons M&A fails. Buyers sometimes focus too much on financial statements and not enough on customer quality, contract terms, technology debt, compliance exposure, employee retention, and operating risk.

McKinsey gives an example from the banking M&A space. Due diligence on the target’s customers would have shown that many were heavy branch users and therefore more likely to leave if branches closed after integration.

McKinsey notes that, in 124 mergers for which it had relevant data, customer losses ranged from 2% to 5% of the combined customer base at the 25th and 75th percentiles.

2. Overvaluation and overpaying

Overpaying can damage even a well-run integration. If the buyer pays a high premium based on aggressive growth, the acquired business must perform almost perfectly after closing.

This is where deal pressure becomes dangerous. A competitive auction, pressure from rivals, and fear of losing a strategic asset can push buyers beyond disciplined valuation. Once that happens, the acquisition starts with a burden: the business must grow into the price.

3. Cultural mismatch

Culture is often discussed too broadly, but in M&A, it has practical effects. It shapes how decisions are made, how managers communicate, how risk is handled, and how fast teams act.

McKinsey research makes the issue more concrete. In a survey of nearly 1,100 M&A leaders, 44% cited a lack of cultural fit and friction between the acquirer and the target company as the top reasons for integration failures.

The real problem is that culture affects daily execution after closing. A fast, founder-led company may struggle inside a process-heavy corporate buyer. A decentralized sales culture may resist a centralized reporting model.

4. Poor integration planning

Integration planning should begin before closing, at least at the workstream level.

Post-close teams need answers to practical questions. Which systems will remain? Who owns customer communication? Which leaders stay? Which products will be retired? How will finance, HR, legal, and IT work together during the first 100 days?

Effective integration planning does not mean making all decisions before the deal closes. Some information will remain limited for legal, regulatory, or competitive reasons. Still, the buyer should know the main workstreams, decision rights, Day 1 priorities, and risks that could affect value.

5. Lack of strategic fit

This often happens in adjacent acquisitions. The buyer understands part of the market but not enough of the target’s daily economics. HBR has warned that related diversification can be risky because companies may believe they understand a target better than they actually do.

For that reason, strategic fit should be tested before valuation becomes emotional. If the buyer cannot explain how the deal will improve the business after closing, it may be more hope than strategy.

6. Weak leadership alignment

Executives need to share a unified view of why the deal matters, what must occur after closing, and who has the authority to make decisions.

A deal can struggle when the CEO, CFO, business unit leaders, and integration team all read the deal thesis differently. One group may expect fast cost cuts, and another may expect growth investment. The acquired team may hear a promise of independence, while corporate leadership expects rapid control.

When those views conflict, decision-making slows. The integration team also has less room to respond when the plan meets resistance.

7. Communication breakdown

Poor communication can quickly erode trust after signing. Employees want clarity on their roles, customers need confidence that service will continue, and suppliers need to understand payment terms and contract continuity.

When leadership stays vague, people fill in the gaps themselves. As a result, rumors spread, key employees may look elsewhere, and customers may delay decisions.

Clear communication does not mean saying everything at once. Instead, it means giving each group the right information at the right time, while being clear about decisions still under review.

8. Regulatory challenges

Regulatory review can delay or reshape a transaction. In some cases, it can stop the deal entirely. Antitrust concerns, foreign investment screening, national security review, industry licensing, and data protection rules can all affect deal certainty.

This risk has become harder to ignore. McKinsey’s 2025 research links longer sign-to-close periods partly to regulatory scrutiny, noting that extended timelines can slow momentum and complicate synergy capture.

For larger deals, a regulatory strategy should be built into the deal plan early. Waiting until late-stage review can weaken negotiation leverage and delay integration planning.

9. Operational inefficiencies

Some acquisitions fail because the buyer underestimates the challenges of running the business after closing.

Operational diligence may receive less attention than valuation work, but it can have a direct effect on deal results. A buyer may negotiate a reasonable price and still lose value if the combined company cannot operate well after closing.

Real examples of failed mergers and acquisitions

Here are four well-known failed mergers and acquisitions, each with a different lesson.

AOL and Time Warner

AOL and Time Warner announced their merger in 2000, near the peak of internet-market optimism. The deal was meant to combine AOL’s online reach with Time Warner’s media assets. Soon after, the dot-com bubble burst, advertising weakened, and the combined company struggled to deliver the expected results.

PBS reported that AOL Time Warner posted a record annual loss after major goodwill write-downs. Other contemporary reporting also described the loss as close to $99 billion.

Daimler and Chrysler

In 1998, Daimler-Benz acquired Chrysler for $36 billion, a deal publicly framed as a “merger of equals.” Although it was presented as a merger of equals, Daimler held stronger control in practice, and the cultural friction was immediate.

The companies had different management styles, operating cultures, and decision-making norms. By 2007, DaimlerChrysler agreed to sell a 80.1% stake in Chrysler to Cerberus for about $7.4 billion.

eBay and Skype

eBay acquired Skype in 2005 for $2.6 billion, with the stated intention of using voice communication to strengthen marketplace transactions. The strategic premise never held up in practice. Skype users had no meaningful reason to use eBay, and eBay sellers had limited use for Skype. The two businesses operated largely independently throughout their combined ownership.

eBay sold a 65% stake in Skype to a private investor group in 2009 for $1.9 billion, while retaining a minority stake. Skype was later acquired by Microsoft in 2011 for $8.5 billion. eBay benefited through its remaining stake, suggesting the asset had real value, just not in eBay’s hands.

Sprint and Nextel

Sprint’s 2005 acquisition of Nextel for $35 billion was expected to create a dominant wireless carrier. Instead, it became a widely cited example of technological incompatibility underestimated during deal evaluation. The two companies operated on different network technologies – Sprint on CDMA, Nextel on iDEN – making integration far more costly and complex than projected.

Combined with leadership turnover and conflicting customer bases, the deal failed to deliver many of its expected synergies.

Sprint recorded a $29.7 billion goodwill impairment related to Nextel in the fourth quarter of 2007, which was reported in 2008. The deal is often cited as a case of why M&A fails when technical due diligence is treated as secondary to financial modeling.

Common problems in post-merger integration

Many failed acquisitions look strong before closing but weak after. Integration exposes the assumptions behind the deal.

Common post-merger integration problems include:

- Cultural clash. Teams may work in different ways, which can slow decisions and increase employee turnover.

- Poor communication. Employees, customers, or suppliers may receive unclear updates, leading to confusion and mistrust.

- Systems incompatibility. Finance, CRM, HR, or reporting systems may not connect, so teams spend more time fixing data than using it.

- Weak Day 1 planning. If leaders do not define what happens immediately after closing, customers and employees may feel the uncertainty first.

- Unclear leadership roles. Slow decision-making often follows when teams do not know who owns key workstreams.

- Overstated synergies. Cost savings or revenue gains may take longer than expected, weakening the deal case.

- Poor data quality. Incomplete or inconsistent data can affect reporting, compliance, and integration planning.

- Delayed customer outreach. If customers hear too little after closing, they may question service continuity or consider other providers.

How to prevent M&A failure

Understanding how to prevent mergers from failing starts with recognizing that many common failure points are preventable. They share common warning signs, and those signs almost always surface during phases when buyers may move quickly and leave important assumptions under-tested.

Improve due diligence processes

A multi-track due diligence process is the most reliable defense against deal regret. Don’t limit the review to documents. Where permitted, speak with customers at multiple levels, interview mid-management, and pressure-test the seller’s revenue assumptions independently.

If something in the data room doesn’t reconcile with what you’re hearing in conversations, slow down. The desire to keep deal momentum shouldn’t override the signals telling you the value you’re paying for may not actually be there.

Align strategy early

Before closing, your leadership team should be able to answer one question with precision: exactly how does this acquisition create measurable value, and how will you track it over 24 months? If that answer requires vague language about synergies or market positioning, the strategic rationale isn’t solid enough yet.

Plan integration before closing

By closing day, you should have a designated integration management office, defined ownership for each workstream, a 90-day operating plan, and an employee communication strategy ready to execute on day one.

Deals that defer integration planning until after close often take longer to stabilize and may cost more than expected. The period between signing and closing is an important planning window, subject to legal and regulatory limits.

Use structured data management tools

Information management during a deal is often chaotic. Centralizing transaction data in a structured, secure environment reduces errors, speeds up review, and protects sensitive information from unauthorized access.

The role of virtual data rooms in successful M&A

Virtual data rooms (VDRs) have become a standard part of many professional M&A processes. They give all parties a centralized, secure environment to share and review documents throughout the due diligence process. For M&A transactions, the organizational benefits can be as important as the security controls

Explore below how virtual data room solutions can support a more controlled M&A process:

- Granular access permissions control which buyers, advisors, lenders, or internal teams can view, download, print, or share specific files.

- Structured folder indexing organizes documents by workstream, such as legal, finance, tax, HR, IT, and commercial diligence, so reviewers can find materials faster.

- In-platform Q&A keeps buyer questions, seller answers, ownership, and response history in one secure place.

- Audit trails track who viewed each document, when they accessed it, and how often they returned to it. This helps deal teams monitor buyer engagement and support accountability.

- Document watermarking adds user details, timestamps, or project information to files to discourage unauthorized sharing.

- View-only and download controls limit copying, printing, or offline access for highly sensitive materials, such as customer contracts or employee data.

- Bulk upload and automatic indexing move large document sets into the data room faster and maintain a consistent folder structure during active diligence.

- Version control helps teams avoid confusion when updated contracts, financial models, or disclosure materials replace older versions.

- Redaction tools hide sensitive details before sharing files with external parties, which is useful for personal data, pricing terms, or commercially sensitive information.

- Reporting dashboards show which folders receive the most attention, which bidders are active, and where diligence may be slowing down.

- A post-close archive preserves the deal record after closing so legal, finance, and integration teams can refer back to key documents when needed.

Conclusion

Most failures trace back to a recurring set of causes: insufficient due diligence, cultural blind spots, strategic misalignment, and integration plans that existed on paper but never got executed with real discipline.

So, regardless of whether this is your first acquisition or your fifteenth, be precise about what you’re buying and why, and have a credible operational plan ready for day one. That won’t eliminate execution risk, but it improves the odds that the deal will deliver the value behind the investment case.

Related posts

11 May 2026

Why do mergers and acquisitions fail? Top causes, examples, and solutions

M&A can create growth, market access, operating scale, and other strategic gains, but the failure record is hard to ignore....

23 March 2026

M&A Data Room Structure: Tips and Checklist

M&A experts highlight that the industry is evolving, despite the drop in deal quantity. According to the PwC 2025 M&A...

13 March 2026

Investment Banking M&A: Key to Successful Deal Execution

M&A is one of the highest stakes in business. These deals can change entire industries. That’s why companies turn to...